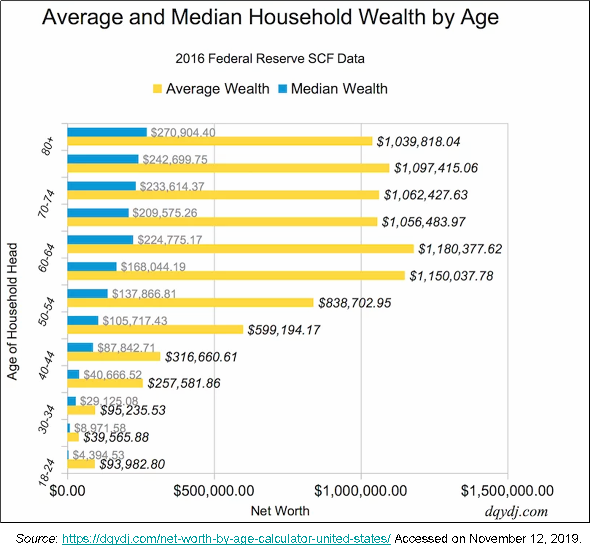

Most of us expect to accumulate wealth as we get older, and with good reason:

Note: Average wealth is total wealth within the age group, divided by number of household heads (main earner) in the age group. Median wealth is the mid-point in the distribution of wealth, meaning half of US household heads in the age group have less wealth and half have more wealth.

How do Americans grow wealth as they get older? This chart tells part of the story:

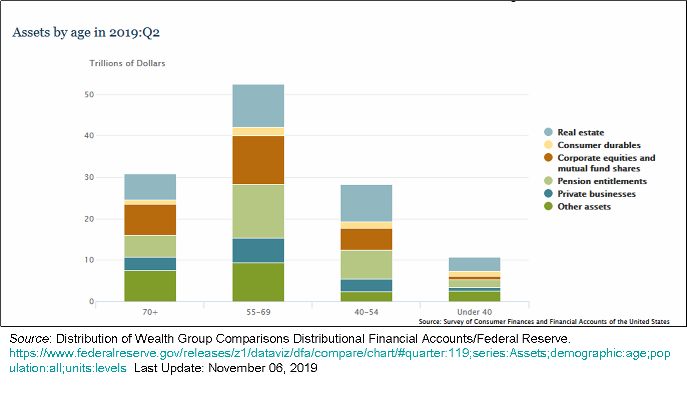

Definitions: Real estate is property made up of land and the buildings on it. Consumer durables are consumer products that do not have to be purchased frequently, like washing machines. Corporate equities reflect ownership shares in corporate businesses. Mutual funds are investment programs funded by shareholders that trades in diversified holdings and is professionally managed..Pension entitlement is the amount of pension which someone has the right to receive when he or she retires..Business asset are items of value owned by a company, such as buildings, machinery, computers, inventory, and intellectual property. Other assets is the miscellaneous category and includes household items like cars, furniture, electronics, and jewelry.

Long story short: household heads under 40 have built up very little wealth, mainly because they don’t have much in the way of home equity or pension entitlements. By middle-age, household heads have twice the wealth of the under-40s, thanks mostly to home equity and pension entitlements (with a nod to corporate equities, mutual funds, and business assets). Wealth peaks in late middle-age/early old age, as financial investments and pension entitlements reach maximum value.

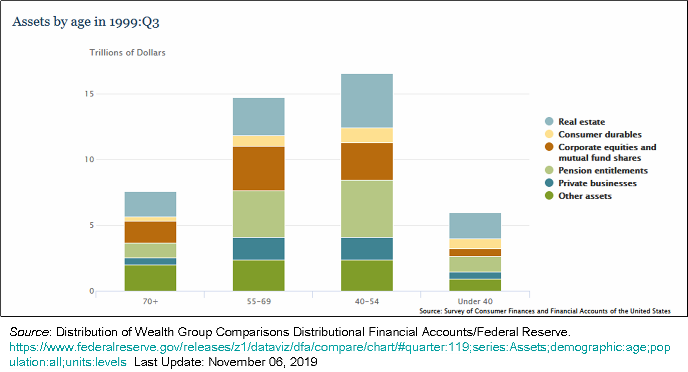

The above pattern of wealth accumulation is relatively new. Check out the 1999 wealth-age breakdown:

Long story short: the age-distribution of wealth in 1999 skews younger than the current distribution . By age 40, household heads had already built up considerable home equity and pension entitlements. Wealth peaked in middle-age, with pensions playing a larger role for that age group than these days. The lower wealth of 55-69 year-old household heads may reflect the period in which many in this group reached working age: the late 1940s-early 1950s, a less affluent time.

Why is it taking longer for today’s under-40 set (aka millennials) to accumulate significant wealth? Mostly because they’re delaying marriage and home ownership, which is partly a result of financial constraints and partly a matter of social change. Compared to previous generations of young adults, millennials are staying in college longer, have higher levels of student debt, and face tighter mortgage lending standards. They also tend to live in cities with nonoptimal housing markets. In other words, millennials are off to a slow start and will have a play a lot of catch-up in the years ahead.

References:

“Distribution of Wealth Group Comparisons Distributional Financial Accounts” Federal Reserve Last Update: November 06, 2019

“The Real Reasons Millennials Aren't Buying Homes” by Aaron Hankin/ Investopedia Updated Jun 25, 2019